Recap: Trade log for the week of April 27

Risk-on week despite the Fed and a wave of Mag 7 earnings. The S&P moved from 7,165 to 7,230, the Nasdaq from 24,837 to 25,114, and VIX cooled from 18.7 to 17.0. Oil kept climbing on the back of the Iran headlines from the prior week, running from $94 to $102 by Friday.

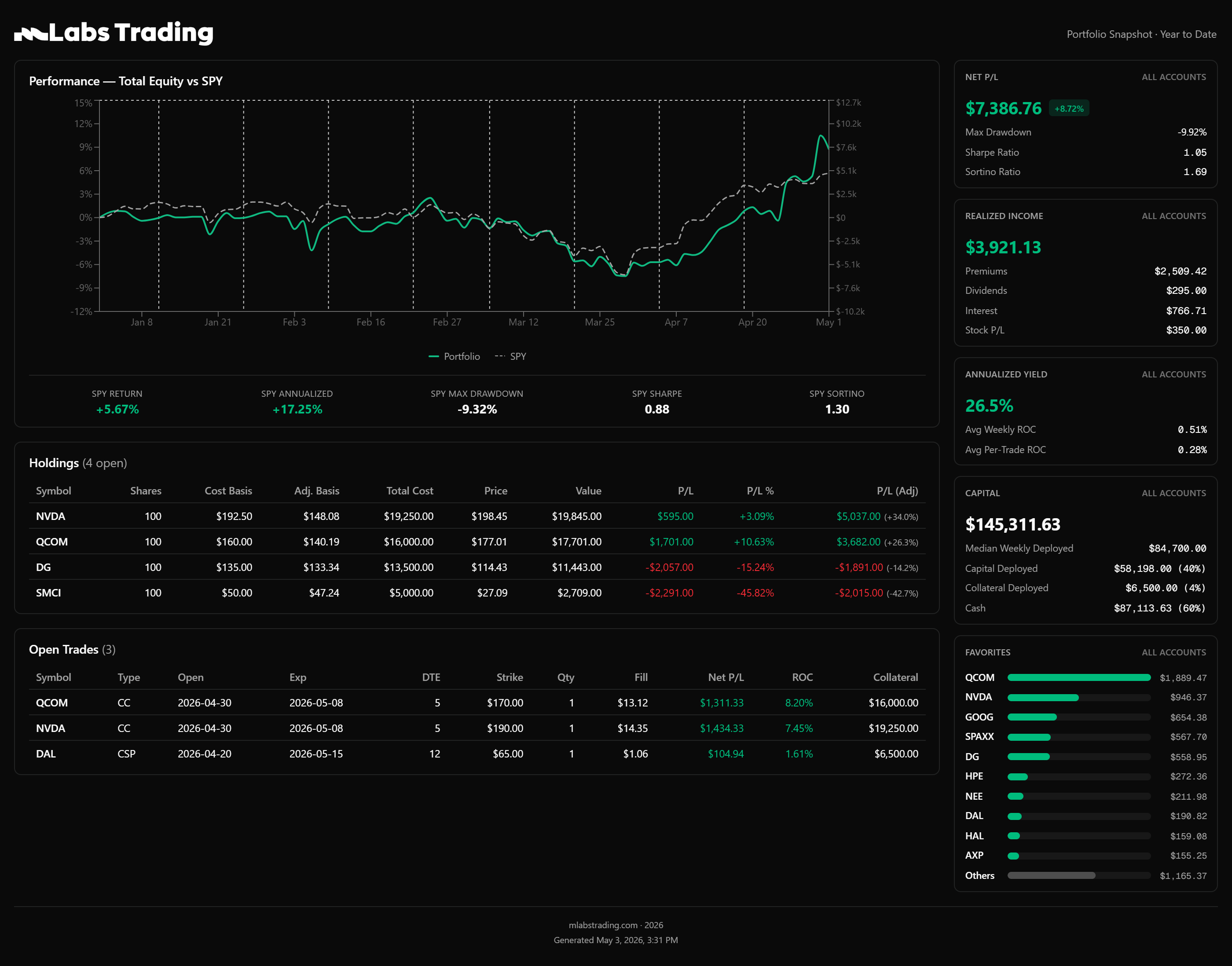

QCOM deserves its own paragraph. We were assigned shares back in mid-January and held them for 108 days through a real drawdown before the stock finally recovered, with one lot getting called away at $170 on Friday and the other still working under a 5/8 $170 CC. Over that stretch we wrote covered call after covered call, collected dividends, and stayed patient instead of panic selling at a loss. This is exactly why we only sell cash-secured puts on names we are genuinely willing to own for months. Boring, quality, profitable companies give you the runway to wait out the chop and let the wheel do its job. Sell puts on garbage tickers and a 108-day hold turns into a permanent loss instead of a winning exit. This is the entire thesis of the strategy in one position.

We opened four positions this week with two of them being rolls. Monday we filled the DVN 5/1 $45.50 cash-secured put as a short-dated energy play. Tuesday we took the C 5/1 $125 CSP into the Fed even though MIQ flagged it Risky, leaning on a Good setup score and intact uptrend. Both puts expired worthless Friday. Thursday we rolled our covered calls out one more week on NVDA and our remaining QCOM lot, writing the 5/8 $190 NVDA CC and the 5/8 $170 QCOM CC at a net credit to capture a bit more premium while IV is still elevated. We are okay with either name getting called away here, that is part of the wheel. The 5/1 $170 QCOM CC on Account 1 expired ITM was called away, locking in the stock gain on top of the premium. The 5/1 $135 DG CC from the prior week expired worthless.

The weekly totals reflect the adjusted picture. The four new opens brought in $2,799 in gross premium, but we had to buy back two covered calls from prior weeks at a loss as the underlyings ran higher, the NVDA 5/1 $190 CC for -$853 and the QCOM 5/1 $170 CC on Account 2 for -$1,071. After also crediting the two prior-week CCs that expired in our favor, net realized for the week comes in at $1,038, or 1.17% ROC on $89,050 of capital deployed. Painful BTCs are part of the wheel when names run, but the underlying stock appreciation more than covers the buyback cost.

The portfolio finished the week at +8.72% YTD with $7,386.76 net P/L, max drawdown at -9.92%, and SPY at +6.42% over the same window. We are now ahead of SPY after sitting in a -7% drawdown back in March. Next week brings the back half of earnings season and a calmer macro slate. We will keep collecting premium while staying boring.

Portfolio snapshot as of May 2, 2026 — click to enlarge

| Type | OpnOpen | Exp | ClsClose | TicTicker | StkStrike | Qty | Fill | ExtExit | Fee | Cap | P/L$ | ROC |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CSP | 4/27 | 5/1 | 5/1 | DVN | 45.5 | 1 | 0.19 | 0.00 | 1.54 | 4.55k | 17.46 | 0.38% |

| CSP | 4/28 | 5/1 | 5/1 | C | 125 | 1 | 0.37 | 0.00 | 1.05 | 12.5k | 35.95 | 0.29% |

| CC | 4/30 | 5/8 | NVDA | 190 | 1 | 14.35 | 0.00 | 0.67 | 19.25k | 580.99 | 3.02% | |

| CC | 4/30 | 5/8 | QCOM | 170 | 1 | 13.12 | 0.00 | 0.67 | 16k | 239.99 | 1.50% |

📥 Download Full YTD Trade Log (CSV)

Open positions from previous weeks that are counted towards deployed capital. These positions did not generate premiums this week.

Closed positions from previous weeks that are counted towards deployed capital. These positions did not generate premiums this week and may have reduced premiums earned from previous weeks.

All trades have been immediately posted in the mLabs Trading Discord community upon execution.

Join the mLabs Trading Discord server

Get notified when we publish new trading insights, results, and strategies.

No spam. Unsubscribe at any time.